April 25, 2018 Honorable Eric Garcetti, Mayor Honorable Michael Feuer, City Attorney Honorable Members of the Los Angeles City Council

Re: Review of the Zoo Department and GLAZA

The Los Angeles Zoo and Botanical Gardens (Zoo) is an important cultural, educational and recreational institution of our City. To help the Zoo best realize its potential, my Office conducted a Review of the Governance Arrangement between the City’s Zoo Department and the not-for-profit Greater Los Angeles Zoo Association (GLAZA). The Review includes recommendations for near-term and long-term changes to propel the Zoo forward.

The Zoo’s mission is to serve Angelenos and visitors by creating a place for recreation and discovery, for inspiring an appreciation for wildlife through exhibitry and education, and for animal welfare. The mission also includes supporting programs that preserve biodiversity and conserve natural habitat. The Zoo has been nationally recognized for its achievement despite staffing shortages, infrastructure challenges and budget limitations. GLAZA, the independent not-for-profit corporation and official support organization of the Zoo, is made up of paid staff and a volunteer board that have been dedicated to managing membership, concessions, fundraising and marketing.

The governance arrangement in which the City’s Zoo Department and GLAZA share responsibilities defined by an operating agreement and multiple Memoranda of Understanding (MOUs), has become cumbersome, however, for all parties involved. The result has often led to confusion and difficulty in fully achieving accountability and transparency. In the near-term, steps should be taken to reduce the confusion and increase accountability. In the longer-term, it is time for the City to explore a new organizational model to make the Zoo the world class entity it can be – and that Angelenos deserve.

The Controller’s Review is based on multiple interviews with officials at the Zoo and GLAZA, and with research of 13 other zoos throughout the country.

Near-Term Recommendations:

Strengthen transparency. While GLAZA exists solely to support the Zoo, it does not publically post its detailed financial transactions – only more general financial reports. To provide more accountability and transparency in line with public expectations, GLAZA should begin to provide the details of its operational revenue and expense transactions online, in line with how the City operates.

Increase accountability. Both the Zoo and GLAZA need to better define and set performance metrics that should be compared against targets, as well as to the performance of prior years and to other similarly sized/situated zoos. Where targets are not being met, there needs to be a process for corrective actions.

Clarify and consolidate multiple agreements. A series of MOUs following the original 1997 operating agreement between the City and GLAZA sought to create a structure to grow programs and activities while and grow support for the Zoo. Collectively, however, these governing agreements have created ambiguity and inconsistencies. It is critical to the success of the Zoo that these agreements be streamlined, so as to better clarify the relative responsibilities and sharing of revenues by the parties.

Longer-Term Recommendations:

While addressing the areas above will help to improve the operational relationship between the Zoo Department and GLAZA, the City will be better served by an alternative organizational model.

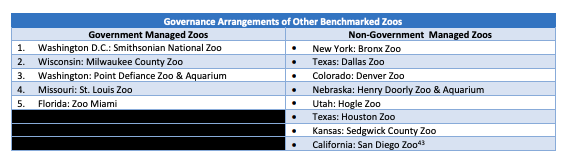

Los Angeles’ current governance structure is unique among zoos. According to a recent study of the Association of Zoos and Aquariums, more than 80 percent of its accredited zoos are non-government managed – and largely operated by not-for-profit entities.

Other cultural entities in Los Angeles County have successfully transitioned their governance arrangements, leading to more prosperous organizations. The Los Angeles County Museum of Art (LACMA), for example, is run by a not-for-profit under a 99-year contract with the County. The LACMA director remains a County employee and is also the Chief Executive Officer of the not-for- profit. The Natural History Museum (NHM) is also run by a not-for-profit with some of its leadership appointed directly by the County Board of Supervisors. There are clear hurdles for the City, many of which are detailed in my report. However, there are also historic examples of success, which should be examined to assist in providing a path forward.

Every year, nearly two million people visit the Los Angeles Zoo and Botanical Gardens (Zoo) for recreation, discovery, and inspiration. The Zoo is an important asset for the Los Angeles region and is part of the City’s cultural, educational, and recreational fabric.

The Zoo is a City Council–controlled Department that was created by Ordinance. A citizen Board of Zoo Commissioners advises the Zoo General Manager (also known as the Zoo Director), who is responsible for control and management of the Zoo Department.1 The Zoo’s Mission Statement is “To serve the community, the Los Angeles Zoo will create an environment for recreation and discovery; inspire an appreciation of wildlife through exhibitry and education; ensure the highest level of animal welfare; and support programs that preserve biodiversity and conserve natural habitat”. In addition, the Zoo’s Vision Statement is “We will leverage the diverse resources of Los Angeles to be an innovator of the global zoo community, creating dynamic experiences to connect people with animals.”

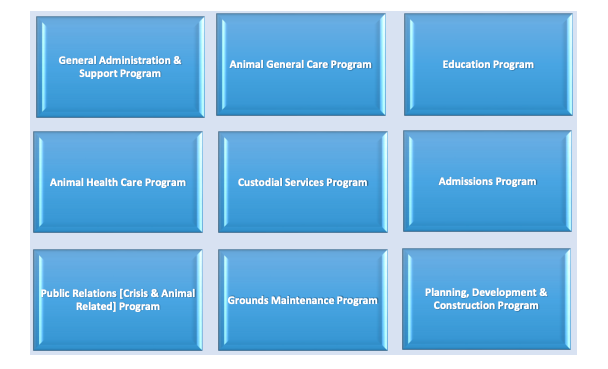

The City’s Zoo Department manages programs related to animal care, admissions, custodial services, grounds maintenance, planning and construction, public relations (crisis and animal related) and general administration. The Greater Los Angeles Zoo Association (GLAZA) is the official support organization of the Zoo, and is an independent not-for-profit corporation. Through the terms of an Operating Agreement, Concession Agreement, and four Memorandums of Understanding (MOUs), GLAZA manages programs related to Zoo memberships, publications, volunteers, concessions, marketing, public relations, special events, and financial assistance [fundraising]. Together, the City’s Zoo Department and GLAZA represent the total Zoo operations and organization.

The Zoo Department’s operating budget is set through the City’s annual budget process, and for Fiscal Year (FY) 2017 totaled $33.4 million. Direct costs of $20.4 million (including staff salaries, animal food, maintenance materials and supplies, contractual services, veterinary supplies, office supplies, uniforms, field equipment, etc.) are covered by an allocation from the Zoo Enterprise Trust Fund (ZETF). The Zoo Department’s indirect and related costs of $13 million (including pension and other human resource benefits, workers compensation, liability claims, and other City overheads) are absorbed by the City’s General Fund.

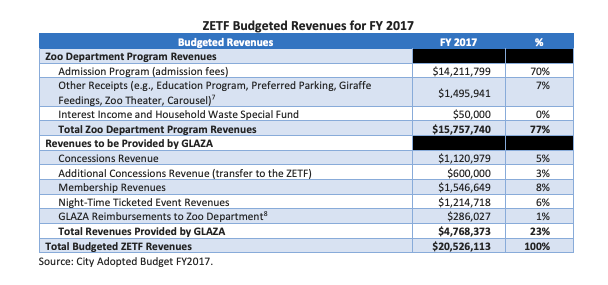

Funds available in the ZETF, a City Special Revenue Fund, derive from revenue receipts collected from Zoo Department programs (primarily admission fees), as well as a portion of the shared revenues from GLAZA-managed programs. Per the FY 2017 adopted budget, 77% of the ZETF’s anticipated revenues come from Zoo Department programs ($15.7 million); while 23% will come from GLAZA ($4.7 million).

1 All but one member of the Zoo Commission is appointed by the Mayor whose terms are five years in length. The Zoo Commission also includes an ex officio member who is chosen by the Chair of the GLAZA Board of Trustees. The ex-officio member serves on the Commission until replaced by the Chair of GLAZA’s Board of Trustees.

Based on GLAZA’s audited financial statements, GLAZA has generated an average of $15.9 million annually over FYs 2014, 2015, and 2016 through the Zoo programs it manages, which includes revenue generated from membership, concession, and fundraising activities. During this period, GLAZA expended an average of $15 million annually. Approximately 35% of GLAZA’s expenditures represent transfers to the ZETF or expenditures Zoo Department management requested GLAZA to make on their behalf from two funds set aside and maintained by GLAZA for the Zoo Department. The remainder were expenditures incurred for program services delivered or performed by GLAZA on behalf of the Zoo (43%), and administrative (13%) and fundraising (9%) activities.

Objective

The primary objective of this special review was to assess whether the current governance arrangement between the Zoo Department and GLAZA has been effective in supporting the achievement of its vision to “leverage the diverse resources of Los Angeles to be an innovator of the global zoo community, creating dynamic experiences to connect people with animals.”

Favorable Conditions Noted

The Zoo has been accredited by Association of Zoos & Aquariums (AZA) for the last 25 years, and has received multiple awards and bred several rare animals during this time. In 2017, the AZA re-accredited the Zoo for another five years and the AZA Visiting Committee indicated they were particularly impressed with the Zoo’s: a) giant river otter exhibit; b) living amphibians, invertebrates, and reptiles exhibit; c) the California Condor Conservation Program; d) the Behavioral Enrichment Program; and, e) the ongoing, close working relationship between the Zoo Department and GLAZA. The AZA Visiting Committee indicated that this close working relationship has been instrumental in the success of the Zoo.

For more than fifty years, GLAZA has funded exhibits, plant and animal species conservation, capital projects, and education and community outreach programs at the Zoo. GLAZA’s Board includes seven Officers and more than 30 other Trustees2; volunteers who bring their public presence, commitment, personal network, and resources to guide GLAZA in its mission and to seek and provide financial support for the Zoo’s programs and capital projects. GLAZA recently completed funding its nearly $20 million commitment to the Elephants of Asia exhibit, significantly increased number of Zoo night-time events and associated revenue, and began fundraising for a new multi-million dollar park. On March 22, 2018, GLAZA provided a letter (included in Appendix IV) that highlights additional favorable conditions.

2 Between FYs 2014 and 2016, GLAZA’s Board of Trustees included from 30 to 38 members.

Conditions Requiring Attention

Prior City audits and other independent reviews have identified concerns at the Zoo in terms of governance, contractual arrangements, oversight, and funding – issues that still persist today. While researching the governance arrangements of other zoos throughout the nation and cultural institutions here in Los Angeles County, we learned that the Zoo’s governance arrangement is unique and in our opinion, it is the primary cause for concerns identified during this special review and the reason the Zoo continues to experience many of the same challenges it has in the past, including Zoo Department staffing shortages and infrastructure and maintenance shortcomings.

We offer several recommendations to enhance accountability and transparency under the current structure. However, we believe an alternative governance arrangement warrants consideration to allow the Zoo to maximize its potential and become the world class Zoo it aspires to be. We recognize this will not be a simple endeavor and will take multiple conversations and negotiations with key stakeholders; but to truly support the achievement of the Zoo’s vision, to “leverage the diverse resources of Los Angeles to be an innovator of the global zoo community, creating dynamic experiences to connect people with animals”, while remaining a safe and affordable family destination for Angelenos and surrounding communities, change is needed. Recommended actions to be taken in the near term and long term are discussed below.

Near Term

Accountability & Performance Metrics: The agreements with GLAZA (i.e., Operating Agreement, Concession Agreement, and four MOUs) do not specify the extent of oversight the Zoo Department is required to provide over GLAZA. Based upon our review and confirmed through interviews, Zoo Department oversight of GLAZA has been limited as the Zoo Department has significant staffing shortages. Our review found that the agreements (i.e., Operating Agreement, Concession Agreement, and four MOUs) contained few metrics, and they are insufficient to monitor GLAZA’s performance. In the near-term, we recommend the Zoo Department, working with the assistance of the Office of the Chief Legislative Analyst (CLA) and the Office of the City Administrative Officer (CAO), in consultation with GLAZA, establish a robust set of metrics tied to City expectations for GLAZA’s performance related to its contractual responsibilities and the intention of the GLAZA Board to support the Zoo’s overall success. Performance results should be compared against targets, as well as to the performance of prior years and to other similarly sized/situated zoos. Noted differences in planned versus actual results should be analyzed and addressed. This review includes suggested data points that could be used to develop performance metrics.

In addition, as significant revenue is realized through the outsourced Concession Program that is currently managed by GLAZA, stronger controls and reporting are necessary to ensure the completeness and accuracy of the reported revenues. Further, our Office supports additional creative strategies now and in the future to maximize revenues to be used for Zoo operations.

Public Transparency: In recent years, the City has dramatically increased its transparency by publicly posting significant amounts of financial information on its website, including detailed transactions related to payroll, purchases, revenues, etc. The public expects accountability of government and public institutions through financial transparency.

Charitable not-for-profits also embrace the values of accountability and transparency as a matter of ethical leadership, legal compliance, and to help preserve the very important trust each donor places in a not-for-profit organization with their contributions. Although GLAZA is a separate entity from the City, it exists for the purpose of establishing, developing, beautifying, and improving the Zoo. Currently, while GLAZA exists solely to support the Los Angeles Zoo, it does not publically post its detailed financial transactions, though high-level summary financial information is available online through its U.S. Internal Revenue Service (IRS) information returns and audited financial statements. To provide more accountability and transparency in line with public expectations, similar to the City and Zoo financial transaction details provided on the Controller’s website via ControlPanel LA, GLAZA should begin to provide the details of its operational revenue and expense transactions online, to be as financially transparent as the City and the Zoo Department. Donors, GLAZA members, and all Angelenos should have access to the amount and type of detailed financial transaction information transparently provided by the City, as GLAZA is an integral part of the City’s Zoo operations.

Further, the transparency of agreements with GLAZA can be enhanced by delineating the value of “in-kind” support (e.g., facilities, staff support, value of free admissions for members, value of merchandise discount for members, etc.) being provided by the City and GLAZA. This practice would also help to ensure that City management has negotiated revenue-sharing terms with GLAZA that are mutually beneficial.

Consolidation & Clarification of Agreements: The Zoo Department and GLAZA are operating from six different agreements (i.e., Operating Agreement, Concession Agreement, and four MOUs) that lack clarity and contain inconsistencies, especially regarding revenue-sharing terms. Further, for many years the Zoo Department and GLAZA have operated from expired MOUs and we found that the Zoo Department has informally authorized departures from certain MOU specifications.

While the overarching 1997 Operating Agreement between the City and GLAZA provides the legal framework for the operational responsibilities of GLAZA, subsequent MOUs have added programs and redefined expectations regarding the financing of Zoo programs and activities.

During initial meetings with the Zoo Director and GLAZA President, both indicated that there is much ambiguity and inconsistency amongst the Operating Agreement, Concession Agreement, and MOUs that needs to be clarified. This review strongly echoes this sentiment and identifies areas in which the Zoo Department could receive additional revenues for its operations. Representatives from the Zoo Department, Office of the City Attorney (OCA), CLA, CAO, and GLAZA should work together to renegotiate, streamline, and clarify GLAZA’s responsibilities and revenue-sharing terms.

Long Term

A New Governance Arrangement: While addressing the three areas above would help to improve the operational relationship between the Zoo Department and GLAZA, in the long term, we believe that the City can best help the Zoo through implementing a new organizational arrangement for governing the Zoo.

While nearly all public zoos partner with a not-for-profit organization to help fundraise, it is an entirely different situation when that not-for-profit manages additional programs for the public zoo and shares in related revenues, but does not exercise operational control or authority. Such an arrangement can generate governance confusion, and in our opinion, this is the situation that exists here for the Los Angeles Zoo.

Other zoos have dealt with this issue either by restricting the role of the not-for-profit to fundraising and community relations, or by allowing a non-government entity (typically a not- for-profit) have near/total control of all zoo operations, even if that non-government entity continues to receive public funding or remains subject to oversight from publicly appointed trustees and board members. It is worth noting that based upon a recent AZA study, the vast majority (81%) of AZA accredited zoos are non-government managed. Further, it appears, based upon best practices and literature, zoos function optimally when managed and governed independently, while engaged in partnership with various levels of government to ensure continued public financial support. One well-known zoo-consulting firm noted that all but six AZA-accredited zoos receive some form of government subsidy, with the average subsidy of 30%- 35% of total revenues. Further, based upon discussions with Zoo Department and GLAZA management, the public is less willing to donate to the Zoo because it is part of City government.

The City has shown a willingness in the past to explore other organizational models. For example, in 2012, the City attempted to change the Zoo’s governance arrangement from being managed by a City Department, to being managed by a not-for-profit entity. A consultant retained by the City indicated that a non-government managed arrangement could reduce the Zoo’s costs and increase revenues through a combination of increased flexibility, increased fundraising opportunities, and the gradual transition of City employees to not-for-profit employees through attrition. The City issued a request for proposal (RFP) to transition the Zoo to non-government management and GLAZA’s proposal was selected. However, the efforts toward transitioning the Zoo to non-government management ceased when the OCA identified several obstacles, including concerns raised by labor regarding the supervision of Zoo employees by a non-City supervisor. As such, future efforts to evaluate alternative governance arrangements should include the input of the City’s labor representatives.

The result of the City’s remaining with the status quo is that the Zoo continues to experience many of the same challenges that it has in the past, including staffing shortages, infrastructure shortcomings and a ZETF fund balance that has decreased substantially, from $10.4 million in FY 2008, to $3.1 million in FY 2017. This is concerning, since the City General Fund subsidy only pays for the Zoo’s indirect operating costs, thus, the ZETF needs to be maintained at sufficient levels to ensure adequate support to pay the Zoo’s direct operating costs.

Conclusion

The results of this review support the position that changes are needed in both the near term and the long term if the Zoo is to truly thrive. The Zoo is a publicly prized asset and it should operate under the conditions that would be most conducive to it reaching its full potential. The current governance arrangement in place, in which the City’s Zoo Department and GLAZA share responsibilities defined by an operating agreement and multiple MOUs, has become cumbersome for all parties involved, contributes to confusion, and makes accountability and transparency difficult to achieve. Beyond this, it is not the model which will allow the Zoo to maximize its potential and become the world class Zoo it aspires to be.

To enable transformative change and to support the Zoo, City policymakers should establish a working group with members from the Mayor’s Office, the CAO, CLA, OCA, representative Council Offices, the Zoo Department, other applicable stakeholders, including labor representatives.

This working group should first work to establish a clear vision of where the Zoo should be in the next 20 years, and then evaluate alternative governance arrangements noted in this report (e.g., the Los Angeles County Museum of Art (LACMA), the St. Louis Zoo, etc.), including the opportunities for enhanced funding and flexibility associated with each arrangement, to determine which will be in the best interest of the Zoo. Subsequently, the working group, with support from policymakers, should identify and implement the steps necessary to transition the Zoo to the most optimal governance arrangement.

Ensuring a stable source of funding for the Zoo is essential, and some form of public subsidy may always be necessary. Nonetheless, the City must determine which of these will best support the Zoo and enable it to thrive and fully realize its vision to “leverage the diverse resources of Los Angeles to be an innovator of the global zoo community, creating dynamic experiences to connect people with animals,” with the Zoo continuing to remain a safe affordable family destination for Angelenos and surrounding communities for years to come. The City must then commit to following through on implementation of its chosen course of action.

Review of Report and Action Plan

A draft of this report was provided to Zoo Department and GLAZA management on February 13, 2018, and we met with Zoo Department and GLAZA management to discuss their comments related to the draft report on March 13, 2018. Auditors considered these comments as we finalized this report.

On March 22, 2018, both the Zoo Department and GLAZA provided formal responses and an action plan, with the intention of them being included as an Appendix to this report (Appendix VI). Based our evaluation of their response, we now consider one recommendation Implemented (No. 5); while three recommendations remain In Progress (Nos. 1, 3, and 4); and two recommendations remain Not Yet Implemented (Nos. 2 and 8).

The Zoo Department and GLAZA disagreed with Recommendation No. 6 pertaining to increasing transparency of the agreements by delineating the value of “in-kind” support (e.g., facilities, staff support, value of free admissions to members, value of merchandise discounts for members, etc.) provided by the City to GLAZA. We believe that quantifying and disclosing “in-kind” support would also help to ensure that City management has negotiated mutually beneficial revenue- sharing terms with GLAZA. However, Zoo Department and GLAZA management indicated that it would require significant effort to identify and itemize the estimated dollar value of “in-kind” support provided between the two organizations, and questioned the cost-benefit of such an endeavor.

GLAZA also disagreed with Recommendation No. 7, to make publically available via the internet, all detailed transactions related to its payroll expenses, purchases, revenues, etc., –similar to type of City and Zoo financial transaction details provided on the Controller’s website via ControlPanel LA. GLAZA indicated that it is a private, not-for-profit entity governed by its Board of Trustees, whose Audit Committee supervises and accepts its annual independent financial audit and IRS Form 990, noting that it now posts those documents on the Zoo’s website. While GLAZA may not be required to publically share its detailed transaction-based information, it exists solely to support a government entity –the Los Angeles Zoo. As such, the Controller believes that it should provide the same level of detailed financial transparency that the City (including the Zoo Department) makes available to the public.

Recommendation No. 9, relates to the exploration of an alternative governance arrangement for the Zoo. It is addressed to City Policymakers for consideration.

We would like to thank Zoo Department and GLAZA staff and management for their time and cooperation during this review.

This section discusses the evolution of the Los Angeles Zoo and Botanical Gardens (Zoo), its management by the City’s Zoo Department, and the evolving role of GLAZA in supporting the Zoo through its significant financial contributions and expanded roles. Understanding the relationship between the Zoo Department and GLAZA lends important context to understanding the Zoo’s current governance arrangement and the issues noted by this review.

History of the City’s Zoo

The City’s first Eastlake Zoo dates back to 1885 in East Los Angeles Park. In 1912, the City’s Griffith Park Zoo opened near the site of the current Zoo grounds. By 1956, it became apparent that the City had outgrown the small Griffith Park Zoo, and voters approved a $6.6 million bond measure to help build a new, expanded Zoo. The Los Angeles Zoo and Botanical Gardens opened at its current location in 1966; until 1997 the Zoo was operated by the City’s Department of Recreation and Parks.

In 1997, City policymakers added Los Angeles Administrative Code (LAAC) §22.700 by ordinance, which created a separate Council-controlled Zoo Department. This code section prescribes that the Zoo Department “shall operate, manage, maintain and control” of the Zoo. A Board of Zoo Commissioners, appointed by the Mayor, advises the Zoo Director. The Zoo Commission meets on a monthly basis with Zoo Department and GLAZA management, often including presentations on GLAZA’s fundraising efforts and significant events occurring at the Zoo.

Today, the Zoo is home to more than 1,100 mammals, birds, amphibians, and reptiles representing more than 250 different species, including 29 endangered species. In addition, the Zoo’s botanical collection comprises several planted gardens and 800+ different plant species with more than 7,400 individual plants. As previously mentioned, the Zoo is accredited by the AZA, an organization that requires the “highest standards of animal management and husbandry, while also focusing on animal management for conservation, education, scientific inquiries, and guest services” and it has continuously accredited the Zoo for more than 25 years.3

Mission and Vision Statements

The following is the Zoo’s mission statement: To serve the community, the Los Angeles Zoo will create an environment for recreation and discovery; inspire an appreciation of wildlife through exhibitry and education; ensure the highest level of animal welfare; and support programs that preserve biodiversity and conserve natural habitat.

The following is the Zoo’s vision statement: We will leverage the diverse resources of Los Angeles to be an innovator of the global zoo community, creating dynamic experiences to connect people with animals.

In 1963 GLAZA incorporated as a not-for-profit organization to assist the City in establishing, developing, and improving the Zoo through fundraising. In 1997, when the City created the separate Zoo Department, the City entered into an Operating Agreement with GLAZA that officially defined its relationship with the Zoo Department.4 According to this agreement, the “Zoo Director shall be exclusively responsible for the administration and management of the Zoo within the policy guidelines set forth by the Mayor and City Council.” GLAZA’s primary responsibility is “to seek and provide financial support to the Zoo and to fund the Zoo’s capital improvements.” Further, “GLAZA shall be responsible, under the terms of the [Operating Agreement], to raise an amount, negotiated yearly, of the Zoo’s annual operating budget and funding needs for capital improvements.”

Appendix I delineates GLAZA’s contributions toward Zoo capital improvements completed between 2000 and 2014.

The organization chart, below, depicts the Zoo Department and GLAZA’s placement within the City’s governance structure.

4 This Operating Agreement will expire in 2022.

The Operating Agreement allows the Zoo Director to contract with GLAZA to perform additional responsibilities for the Zoo through separate MOUs.5 As of October 2017, under the Operating Agreement, Concession Agreement (distinct from the Concessions MOU), and four separate MOUs, GLAZA supports the Zoo Department by managing the following programs:

As of October 2017, GLAZA has 40 full time and 26 part time employees. The number of part time employees fluctuates seasonally. See Appendix II for a fuller description of GLAZA’s responsibilities per the referenced MOUs.

5 The Operating Agreement specifies that the City may contract through a separate MOU for GLAZA to perform the Zoo Department’s responsibilities for publications, special events, and the rental, construction, operation and maintenance of Zoo facilities. It also specifies that all separate MOUs entered into between GLAZA and the Zoo Department will operate as “sub-agreements” to the Operating Agreement.

The Zoo Department manages the remaining programs as part of its regular operations: 6

As of October 2017, the Zoo Department has 219 full-time employees and it has the ability to use 133 part-time positions, as needed. For City budgetary purposes, the Zoo Department has position authority for 246 full time positions (233 regular authority and 13 resolution authority). See Appendix III for a fuller description of the Zoo Department’s programs and activities.

6 GLAZA public relations staff work with Zoo Department public relations staff to ensure consistent messaging in Zoo communications.

Zoo Department Funding

As a Council-controlled City Department, the Zoo Department is subject to annual budget appropriations to fund operations. For FY 2017, the City budget allocated $33.4 million for the Zoo Department.

$20.4 million (61% of the Departmental budget) represents direct operating costs (staff salaries, animal food, maintenance materials and supplies, contractual services, veterinary supplies, office supplies, uniforms, field equipment, etc.). All direct costs are covered by the Zoo Enterprise Trust Fund (ZETF), a City Special Revenue Fund that receives and allocates funds that are restricted for Zoo purposes. The remaining $13 million represents the City’s budgetary allocation of indirect and related costs (pension and human resource benefits, workers compensation, liability claims, and other City overheads) associated with the Zoo Department, which is covered by the General Fund.

Funds available in the ZETF are generated from Zoo Department receipts (primarily admission fees) and a portion of revenues generated by GLAZA for their managed programs, as transferred to the City. For FY 2017, the Zoo Department’s adopted budget indicated 77% of ZETF revenues would come from the Zoo Department programs; while 23% would come from GLAZA, as an allocation of shared revenues under terms of the Operating Agreement, Concession Agreement, and MOUs. See the Table below.

7 Prior to February 2017, GLAZA operated the carousel.

8 GLAZA reimburses the Zoo Department when its employees work overtime at night-time ticketed events.

In addition to the City budget, the Zoo Department has access to funds held in two accounts maintained by GLAZA: the Zoo Assistance Fund (ZAF) and the Zoo Surplus Development Fund (ZSDF). These accounts, specifically mentioned in two MOUs, are held by GLAZA for the direct benefit of the Zoo Department, i.e., operating costs not funded through the City budget.9 Specifically, the Financial Assistance, Special Events, and Community Affairs MOU specifies that GLAZA is to transfer a “gift” of unrestricted fundraising revenues into the ZAF each year. And while the Concessions MOU specifies that GLAZA is to transfer any excess commissions revenue into the ZSDF, based upon a suggestion by the CAO, since FY 2015 the Zoo Department annually transfers $600,000 (a majority of ZSDF monies) to the City’s ZETF.

See Appendix IV for a schedule delineating revenues collected per MOU and distributions to the ZETF, ZAF, and ZSDF.10

GLAZA Funding

As the official support organization for the Los Angeles Zoo & Botanical Gardens, GLAZA is an independent not-for-profit corporation organized for the purpose of establishing, developing, beautifying and improving the Zoo. While GLAZA is exempt from income taxes, it files an annual informational return per IRS requirements, and provides an Independent Audit of its annual financial statements to its Trustees and began posting its audited financial statements to its website in April 2017.

Based on GLAZA’s audited financial statements for FYs 2014, 2015 and 2016, GLAZA generated an average of $15.9 million per year in support and revenues. Sources are attributable to membership program revenue (37%), contributions and grants (30%), and visitor amenities (19%), with some additional revenues from special events net of direct donor benefits, and investment income.

During this same period, GLAZA expended an average of $15.0 million each FY. On average, 35% represented transfers to the ZETF or expenditures Zoo Department management requested GLAZA to make on their behalf from two funds (the ZAF and ZSDF mentioned above) maintained by GLAZA for the Zoo Department. The remainder were expenditures incurred for Zoo program services delivered or performed by GLAZA on behalf of the Zoo (43%), general and administrative (13%), and fundraising (9%) activities.

9 According to Zoo Department management, the ZAF and ZSDF are used for operating costs that are not funded through the City budget, and the monies in these accounts are typically spent by the end of each FY. The ZAF primarily funds conservation and research programs. ZSDF monies not transferred to the ZETF are primarily used for animal care equipment and supplies, training, travel, visitors’ surveys, etc. While both the ZAF and ZSDF amounts are held by GLAZA, Zoo Department management indicated that they control the use of the monies in these accounts by requiring approval signatures from the Zoo Department’s Chief Management Analyst and Assistant General Manager and/or General Manager.

10 The Operating Agreement and Concession Agreement also specify how GLAZA apportions shared revenues with the Zoo Department. As mentioned in the Consolidation and Clarity of Agreements section, certain Operating Agreement and Concession Agreement specifications conflict with MOU specifications and certain MOU specifications conflict amongst each other.

As of June 30, 2017, GLAZA’s assets included $29.5 million in combined cash, cash equivalents and investments; $4 million in receivables; and $763,000 in other assets. GLAZA’s net assets totaled $31.3 million, of which $21.5 million (69%) was unrestricted11, $7.7 million (25%) was temporarily restricted; and $2.1 million (7%) was permanently restricted.

Prior Audits & Reports

Concerns regarding the City’s administration of agreements with GLAZA stretch back for decades, even before the City created the Zoo Department in 1997. In fact, in 1990 when the Los Angeles County Grand Jury evaluated the City’s relationship with GLAZA, the Grand Jury reported multiple findings but two remain relevant to our current review. Specifically, the Grand Jury found: 1) the prior Operating Agreement and current Concession Agreement had been poorly written; and, 2) the City did not exercise its authority to audit and monitor concession operations, nor did it independently audit concession receipts. The Grand Jury concluded that “weak management” and certain provisions in the agreements with GLAZA hampered the City’s ability to “fulfill its duty to manage the Zoo.”

In December 2002, the Controller’s Office issued its “Report on the Greater Los Angeles Zoo Association” that identified subpar fundraising performance by GLAZA and a potential over- retention of millions in revenues due to the City from the Membership Program and Concessions Program. At the time, both GLAZA and the new interim Zoo Director disagreed with the audit’s finding regarding the shared revenues.

Subsequent audits by the Controller’s Office in 2005 and 2009 noted that recommendations relating to the City Attorney providing a legal opinion on the possible over-retention of shared revenues remained outstanding, and noted the Zoo Department and GLAZA had been operating from expired MOUs. The 2009 audit also recommended the Zoo Department complete a cost- benefit analysis on the feasibility of directly contracting for concession services. However, due to reported staffing shortages, the Zoo Department did not conduct this cost-benefit analysis.

11 However, $19.2 million was Board-designated for endowment and certain projects.

While evaluating the Operating Agreement, Concession Agreement, and MOUs that the City and/or Zoo Department have with GLAZA, we found that they generally lack specification as to the extent of oversight the Zoo Department is expected to provide over GLAZA and their shared revenue arrangements, which include membership, concessions, and site rentals (among others).

The Zoo Department needs to enhance its oversight of GLAZA through increased accountability and the use of a robust set of metrics to monitor GLAZA’s performance.

According to interviews with Zoo Department management, the Zoo Department’s oversight of GLAZA is limited. For example, the Zoo Department does not: 1) compare GLAZA’s reported shared revenues and expenses to GLAZA’s general ledger of historical detailed trial balances; 2) review any of GLAZA’s or GLAZA’s subcontracted Concessionaire’s internal controls to ensure completeness and accuracy of reported shared revenues; 3) review any of GLAZA’s deductions from shared membership or night-time ticketed event revenue; or, 4) require GLAZA to submit a yearly actual versus budget comparisons of shared revenue calculations for each MOU. While it is a City contractor subject to oversight and monitoring by the Zoo Department, GLAZA holds a unique role in its relationship with the Zoo, and is seen more as a partner than a contractor. This has raised questions as to GLAZA’s compliance with the terms of its agreements with the City as delineated in the Consolidation and Clarity of Agreements section of this report.

In addition, although the Concession Agreement requires that the Zoo Department receive: 1) a monthly profit and loss statement on concession sales each month with a breakdown of expenses and net income for concession activity; and, 2) an annual Income Statement and a Balance Sheet for the Concessionaire’s concession operations prepared by an independent Certified Public Accountant, we found that these reports are not being prepared or provided to the Zoo Department and GLAZA. However, these reports would be a good mechanism to help GLAZA and the Zoo Department monitor the Concessions Program and to negotiate revenue-sharing arrangements.12 GLAZA management indicated that it will be issuing a RFP for Concession Services in the near future and the subsequent contract will contain a requirement to provide these reports to the Zoo Department as required by the Concession Agreement.

Further, this review evaluated a small sample of GLAZA expenses deducted from shared membership and night-time ticketed events revenue. While the costs were supported by documentation, we were unable to conclude on the reasonableness of the expenses, as GLAZA’s Accounting Policies, Procedures, and Internal Controls (written policies and procedures) are insufficient. Specifically, GLAZA’s procedures require its managers to “investigate new vendors during the budgeting process and whenever goods and services are needed. For large purchases, department managers obtain quotes from several reputable vendors.” However, the written policies and procedures do not specify what constitutes “large purchases,” how to document and retain RFP submissions and price-quotes, and what type of documentation is required before a vendor can be used and a payment can be issued.

12 The 1981 Concession Agreement required GLAZA to provide the reports described in the preceding paragraph to Zoo Department management. This was when GLAZA directly operated the Zoo’s concessions. In 1997, the Operating Agreement reaffirmed the terms of the Concession Agreement, but allowed GLAZA to subcontract its concession function. GLAZA then entered into an agreement with Service Systems Associates (Concessionaire) effective October 1, 1997 and has managed the Concessionaire since this time; however, its contract with the Concessionaire did not include the requirement to provide the required financial reports to Zoo Department or GLAZA management.

Upon inquiry of Zoo Department management, we learned that they do not have sufficient staffing levels to provide detailed fiscal oversight of agreements with GLAZA. The Zoo Department also has staffing shortages in other critical areas such as animal keepers, maintenance construction helpers, and curators, as delineated in the Long Term Governance of the Zoo section of this report.

Given the lack of staffing to provide detailed fiscal oversight, Zoo Department management could improve accountability by using a robust set of performance metrics to monitor GLAZA’s program and fundraising performance.

Our review of agreements (i.e., Operating Agreement, Concession Agreement, and MOUs) found that they do not include adequate performance metrics to evaluate GLAZA’s performance. For many years, GLAZA and the Zoo Department have operated from expired MOUs, and most of the performance expectations contained therein with the exception of a prior FY 2013 Marketing and Public Relations & Site Rentals/Catered EventsMOU, were based on GLAZA’s budgeted revenues and expenses for the upcoming year. However, in comparing the FY 2013 Marketing, Public Relations, Site Rentals, & Catered Events MOU to the FY 2017 MOU, significant performance metrics were removed. Specifically, the FY 2017 MOU: 1) no longer includes a minimum investment by GLAZA; 2) removed several performance metrics related to expected increases in Zoo revenues; and, 3) authorized a $1.6 million Marketing Refund to GLAZA without it being distinctly tied to its performance. For FY 2017 none of the MOUs contain performance metrics that require comparisons to the results from prior years, or to other zoos to gauge GLAZA’s performance. To drive improvements and focus resources towards reaching a target, it is critical that performance metrics be established to evaluate GLAZA’s performance, as a contractor and fundraiser for the City.

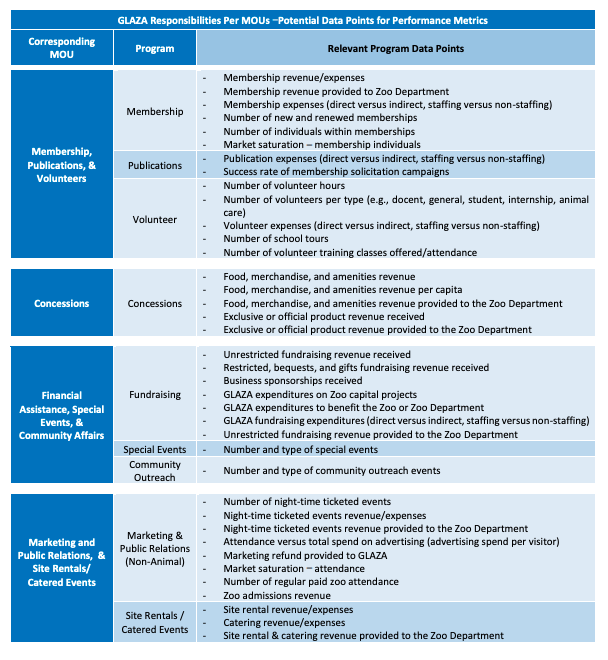

Based upon the programs currently managed by GLAZA, we offer the following potential data points that City management can use to develop goals and performance metrics for GLAZA, that could then be evaluated on a quarterly and a multi-year basis. Different from the metrics that should be used to assess the Zoo’s overall performance toward meeting its strategic goals in its Business Plan, these performance metrics would be focused on evaluating GLAZA’s program and fundraising activities and could be used to compare against prior years and other similarly sized/situated zoos. Any differences in planned versus actual results should be analyzed and addressed. See the following Table for potential data points that could be used to develop a robust set of performance metrics.

Further, regarding GLAZA’s marketing of the Zoo’s Daytime Admissions Program, in a June 21, 2013 memorandum to the City’s Budget and Finance Committee, the CLA questioned whether the transfer of marketing responsibility to GLAZA would financially benefit the City.13 After assuming daytime admissions marketing responsibilities, GLAZA did not meet its performance metrics and as a result, GLAZA did not obtain the full Marketing Refund from the Zoo Department that it anticipated.14 On March 19, 2015, Zoo Department management requested City Council to authorize an amendment to the Marketing, Public Relations, Site Rentals, & Catered Events MOU, allowing GLAZA to include net night-time ticketed events revenue to meet the performance metric originally structured to measure only daytime admissions revenue increases. This metric was used to calculate GLAZA’s Marketing Refund. However, as previously mentioned, the FY 2017 Marketing, Public Relations, Site Rentals, & Catered Events MOU no longer includes performance metrics related to expected increases in Zoo revenues and authorized a Marketing Refund to GLAZA without being distinctly tied to its performance. Although GLAZA has since generated substantially more revenue from night- time ticketed events (e.g., Zoo Lights, Roaring Nights, and Brew at the Zoo), these events represent a new stream of revenue that could have been tracked and measured separately to ensure there is adequate monitoring of projected increases of daytime admissions revenue and attendance.

For a summary of the Zoo’s historical gate attendance from FY 2002 – 2016, see Appendix V.

Recommendations

Insofar as the current governance structure and operational responsibilities exist,

Zoo Department management should:

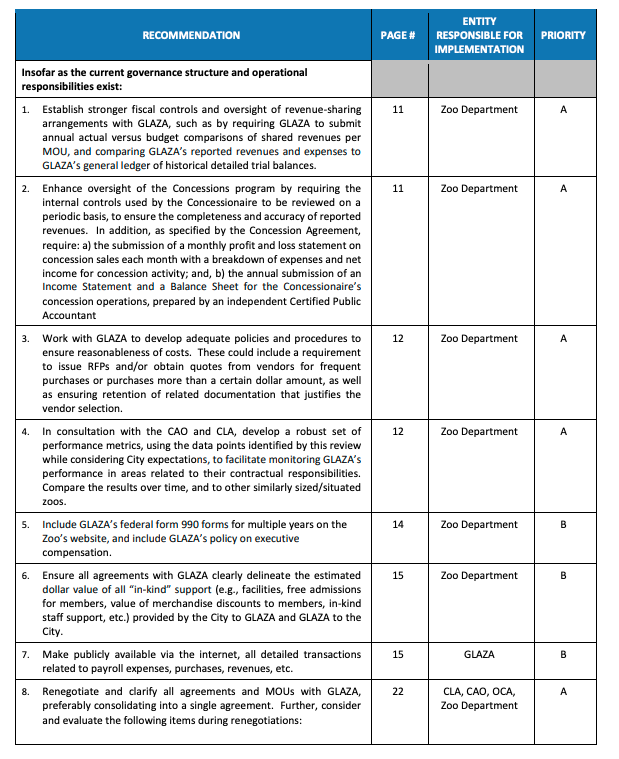

Establish stronger fiscal controls and oversight of revenue-sharing arrangements with GLAZA, such as by requiring GLAZA to submit annual actual versus budget comparisons of shared revenues per MOU, and comparing GLAZA’s reported revenues and expenses to GLAZA’s general ledger of historical detailed trial balances.

Enhance oversight of the Concessions program by requiring the internal controls used by the Concessionaire to be reviewed on a periodic basis, to ensure the completeness and accuracy of reported revenues. In addition, as specified by the Concession Agreement, require: a) the submission of a monthly profit and loss statement on concession sales each month with a breakdown of expenses and net income for concession activity; and, b) the annual submission of an Income Statement and a Balance Sheet for the Concessionaire’s concession operations, prepared by an independent Certified Public Accountant.

13 In the June 21, 2013 memorandum issued to the City’s Budget and Finance Committee, the CLA indicated: “it appears, net revenues from paid admission that are achieved above and beyond what the Department would otherwise retain from annual admission [fee] increases, will revert to GLAZA and will not benefit the City’s General Fund or the Zoo Department directly. Although the MOU projects that the Department will achieve increased revenues from additional membership and concessions, these increases could be realized with increased attendance and would not require the MOU to do so.”

14 In FYs 2014, 2015, and 2016, GLAZA received the following Marketing Refunds: $0, $761,057, and $1,590,540, respectively. The original MOU authorized the Marketing Refunds of up to: $591,596, $1,308,820, and $2,169,074 respectively for each of these FYs based on the amount of anticipated increased revenue to the Zoo Department.

Work with GLAZA to develop adequate policies and procedures to ensure reasonableness of costs. These could include a requirement to issue RFPs and/or obtain quotes from vendors for frequent purchases or purchases more than a certain dollar amount, as well as ensuring retention of related documentation that justifies the vendor selection.

In consultation with the CAO and CLA, develop a robust set of performance metrics, using the potential data points identified by this review while considering City expectations, to facilitate monitoring GLAZA’s performance in areas related to their contractual responsibilities. Compare the results over time, and to other similarly sized/situated zoos.

In recent years, the City has gone to great lengths to increase its public transparency by posting information on its budget, payroll, purchasing, revenue, assets and liabilities, and other statistics. Similarly, the demand for financial accountability by not-for-profit organizations has increased. We identified the need to enhance transparency, not only within the various agreements between the City and Zoo Department, but also with the amount of financial information GLAZA shares with the public.

GLAZA’s detailed financial activities should be made public for Angelenos and donors.

In recent years, the City has dramatically increased its transparency by publicly posting significant amounts of financial information on its website. The public expects accountability of government and public institutions through financial transparency.

Charitable organizations are also embracing the values of accountability and transparency as a matter of ethical leadership, legal compliance, and to help preserve the very important trust each donor places in a not-for-profit through their contribution. Although GLAZA is a separate not- for-profit corporation, it exists for the primary purpose of establishing, developing, beautifying, and improving the City’s Zoo. Currently, even though GLAZA exists solely to support the Los Angeles Zoo, it does not publically post its detailed financial transactions, though high level financial information is available through its annual U.S. Internal Revenue Service (IRS) information returns and audited financial statements.

To provide more accountability and transparency, in line with public expectations, GLAZA should begin to provide the details of its operational revenue and expense transactions online, to be as financially transparent as the City and the Zoo Department.15 Although GLAZA began including their audited financial statements on its website in April 2017, donors, GLAZA members, and all Angelenos should have access to the same amount and type of detailed financial information transparently provided by the City as GLAZA is an integral part of the City’s Zoo operations.

GLAZA management indicated that because it is not a government organization and receives no taxpayer funding, it does not publicize its detailed transactional financial information. Further, management emphasized that GLAZA is an independent not-for-profit organization governed by a Board of Trustees with a fiduciary duty to the organization, and that the Zoo Director attends the Board of Trustees meetings and Board Committee meetings, and is present when GLAZA’s financial matters are discussed.16

15 When initiating this review, GLAZA management sent correspondence to our Office requesting that its General Counsel serve as our point person to process all questions and document requests, and its General Counsel requested to be present during all interviews of GLAZA staff. The correspondence also indicated that as a private organization, GLAZA retained all rights related to privacy laws.

16 GLAZA management also indicated that it fully complies with all state and federal laws regarding not-for-profit reporting and disclosure.

Further, similar to leading practices found with the Huston Zoo and LACMA, the Zoo Department should include GLAZA’s federal 990 forms on its website. LACMA also includes its Policy on Review of Executive Compensation on its website, which serves to enhance public transparency.

Agreements with GLAZA require more transparency.

While reviewing the agreements between the Zoo Department and GLAZA, we found that the Membership, Publications, and Volunteer Programs MOUs for FYs 2012 and 2017 delineated only the total costs of each program that GLAZA was authorized to deduct from shared revenues. These MOUs did not provide a breakdown of direct staffing and non-staffing expense estimates, nor did they provide any indirect staffing and non-staffing expense estimates for each program. Considering that GLAZA has deducted more than $6.3 million, or 61% of its $10.3 million total indirect expenses between FYs 2012 to 2016 from shared membership revenues, this information needs to be delineated to City management, which would also enable the Zoo Department to properly monitor the fiscal sharing arrangements.

Further, we noted that the transparency of agreements with GLAZA can be enhanced by delineating the value of “in-kind” support being provided by the Zoo Department. For example, based upon a review of the MOU between Milwaukee County and the Milwaukee Zoo’s associated not-for-profit, the Milwaukee MOU delineates all the support, including “in-kind” support being provided to the not-for-profit by Milwaukee County and by the not-for-profit to Milwaukee County, quantified into a dollar value. The MOU contains a listing, with estimated dollar values, of the free admissions provided to the not-for-profit’s members, a dollar value of food and merchandise discounts provided to the not-for-profit’s members, facility costs, etc. The Milwaukee MOU also requires that for each capital project, Milwaukee County and the associated not-for-profit execute a separate specific agreement describing sources and uses of funds, procedures for transferring the not-for-profit’s share of project costs to Milwaukee County, program management, project schedule, and other specific arrangements. During our Mach 13, 2018 meeting with Zoo Department and GLAZA management, GLAZA representatives indicated that they believe the inclusion of “in-kind” support in agreements would lead to further confusion, but we believe that the practice of delineating “in-kind” support would help to ensure that the City has negotiated revenue-sharing terms with GLAZA that are mutually beneficial.

Recommendations

Insofar as the current governance structure and operational responsibilities exist,

Zoo Department management should:

Include GLAZA’s federal form 990 forms for multiple years on the Zoo’s website, and include GLAZA’s policy on executive compensation.

Ensure all agreements with GLAZA clearly delineate the estimated dollar value of all “in- kind” support (e.g., facilities, free admissions for members, value of merchandise discounts to members, in-kind staff support, etc.) provided by the City to GLAZA and by GLAZA to the City.

GLAZA management should:

Make publicly available via the internet, all detailed transactions related to payroll expenses, purchases, revenues, etc.

During initial meetings with the Zoo Director and GLAZA President, both indicated that there is much ambiguity and inconsistency amongst the Operating Agreement, Concession Agreement, and MOUs, which need to be clarified and streamlined. This review strongly echoes this sentiment. We recommend that representatives from the Zoo Department, OCA, CLA, CAO, and GLAZA work together to renegotiate, streamline, and clarify GLAZA’s responsibilities and revenue-sharing terms into one agreement. In conducting these renegotiations, we highlight the following areas for consideration.

Poorly written and conflicting terms in agreements (Operating Agreement and MOUs) give rise to questions about GLAZA retaining more shared membership revenue than may have originally been intended.

We found inconsistencies between the Operating Agreement, FY 2012 Membership, Publications, & Volunteer Programs MOU, and the FY 2012 Financial Assistance, Special Events & Community Affairs MOU. The Zoo Department and GLAZA operated from these agreements between FYs 2012 and 2016.17 While the FY 2012 Membership, Publications, & Volunteer Programs MOU authorized GLAZA to deduct a majority (up to 59%) of shared membership revenues for its Membership Program costs, both the 1997 Operating Agreement and the FY 2012 Financial Assistance, Special Events & Community Affairs MOU include terms that appear to limit the amounts GLAZA can deduct.18 Specifically, the Operating Agreement appears to limit GLAZA’s retention of membership fees to 25% for its administrative costs and the FY 2012 Financial Assistance, Special Events & Community Affairs MOU appears to require GLAZA to underwrite all of its indirect expenses (e.g., administrative, information technology, special events, and volunteers etc.).19 20

17 Although the MOUs expired at the end of FY 2012, the Zoo Department and GLAZA agreed to operate based upon the expired MOUs through FY 2016.

18 The MOUs are signed agreements negotiated between the Zoo Department and GLAZA while the 1997 Operating Agreement is a signed agreement that was negotiated between the City and GLAZA.

19 The 1997 Operating Agreement specifies: a) GLAZA may use a portion of fees charged for membership in the Zoo for its administrative costs. From each family, individual, and other membership fee, GLAZA shall retain for such purposes 25% of each fee; b) From each family, individual, and other membership fee, GLAZA shall remit 25% to the City; and, c) The remainder of monies received from membership fees shall be deposited into the City’s ZETF unless the Zoo Director and GLAZA enter into an MOU requiring GLAZA to perform services for the Zoo Department. If the MOU does not allocate the remaining monies received from membership fees, all such unallocated fees shall be deposited into the ZETF.

20 The FY 2012 Financial Assistances, Special Events & Community Affairs MOU specifies: As a result of all its unrestricted fundraising efforts, GLAZA will gift the sum of $365,000 to the Zoo Assistance Fund for public relations, marketing, and conservation efforts, and will entirely [emphasis added] underwrite the costs of the GLAZA departments and activities discussed herein, such as Development, Information Technology, Special Events, Volunteers, and other GLAZA produced or sponsored activities that “complete” the total operations of the Los Angeles Zoo, as well as the costs for finance and administration of GLAZA, including insurance. This term appears to indicate that unrestricted fundraising revenue are to fund GLAZA’s indirect expenses. We noted that GLAZA modified the FY 2016 MOU by removing the word “entirely.” GLAZA management indicated the edit was made to remove inconsistencies with the Membership, Publications, and Volunteer Programs MOU, but we found that Zoo Department management had been unaware of the edit. This occurrence indicates that the Zoo Department needs better controls to ensure all revenue-sharing modifications are agreed upon, and transparently delineated to all parties prior to the agreements’ formal execution.

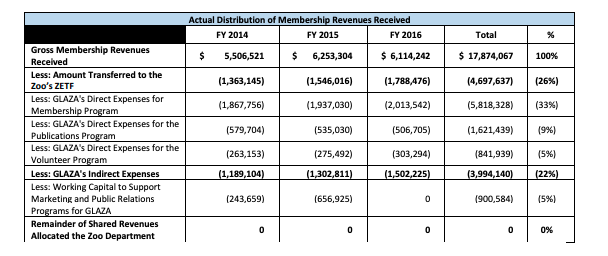

The following table delineates GLAZA’s retention and distribution of shared membership revenue from FYs 2014 to 2016, in which nearly $4 million had been deducted for its indirect expenses.

During FYs 2012 and 2013, GLAZA deducted $1,199,189 and $1,150,411, respectively, from shared membership revenue for its indirect expenses. Thus, between FYs 2012 and 2016, GLAZA deducted a total of $6.3 million ($4.0 million and $2.3 million) for its indirect expenses from shared revenues.

Based upon the terms of the Operating Agreement and the FY 2012 Financial Assistance, Special Events & Community Affairs MOU, it appears that GLAZA should not have deducted its indirect expenses from shared membership revenues between FYs 2012 and 2016. However, since the Zoo Department entered into the Membership, Publications, & Volunteer MOU for FY 2012 with GLAZA, which allowed them to effectively retain 59% of shared membership revenues to offset their expenses, it appears the Zoo Department authorized additional deductions by GLAZA for its indirect expenses.21 22

21 It is also questionable whether shared membership revenues retained by GLAZA for managing the Volunteer Program is allowable.

22 We also noted that GLAZA deducted $6.3 million (61%) of its $10.3 million indirect expenses from shared membership revenues between FYs 2012 and 2016 without having a sound basis to support the deductions. Although GLAZA uses a spreadsheet that allocates percentages of its indirect expenses to the Membership Program, Publications Program, and Volunteer Program, GLAZA management indicated that the percentages had been developed many years ago and they did not have any documentation to support how the percentage allocations were developed.

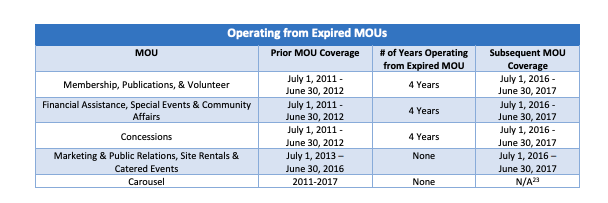

The Zoo Department and GLAZA operate from expired MOUs and certain departures from MOU specifications were not formally documented.

For many years, GLAZA and the Zoo Department have operated from expired MOUs. From FYs 2014 through 2016, the Zoo Department and GLAZA operated from three MOUs that had expired on June 30, 2012. Further, for much of FY 2017, the Zoo Department operated from unexecuted MOUs with GLAZA, with the four MOUs being formally executed only in May 2017, the month prior to them expiring. We believe part of the reason for this occurrence is that most of the MOUs covered a period of one year. See the Table below.

The Zoo’s three-year Strategic Business and Marketing Plan also expired as of July 2017.24 25

Moreover, pursuant to the FY 2012 Membership, Publications, & Volunteer Programs MOU, GLAZA was authorized to deduct $812,308 from shared membership revenue to run the Publications and Volunteer programs. However, GLAZA deducted $1.1 million, $1.1 million, and $1.2 million, in FYs 2014, 2015 and 2016 respectively. Zoo Department management indicated they had been aware that GLAZA was deducting more for these programs each year, even though they did not officially approve the increases or review the specific costs.

23 This MOU expired in February 2017 when the Zoo Department assumed the responsibility for operating the Zoo’s carousel.

24 Per LAAC Chapter 27, Article 1, Section 22.711 the Zoo’s Business Plan must contain marketing and financial projects for the Zoo for a maximum period of 5 years, and include but not be limited to, methods to attract additional visitors and funds to the Zoo and calculations of funds anticipated to be received from fund raising, admissions (paid attendance) at the Zoo, City General Fund, membership, grants, concession(s), and other commercial enterprises.

25 On February 7, 2018, the Zoo Department submitted a one-year Business and Marketing Plan for FY 20-18 to City Council, indicating a multi-year plan will be developed that addresses recommendations contained in this Special Review.

A renegotiation, consolidation, and clarification of all agreements (i.e., Operating Agreement, Concession Agreement, and MOUs) with GLAZA could result in the Zoo Department receiving additional revenue for its operations.

Opportunities to Enhance Shared Revenues with the Zoo Department

Exclusive or Official Product and Service Agreement Revenues. To manage the Concessions Program, GLAZA received $1,037,439 from FYs 2014 through 2016. However, this amount does not include additional revenues GLAZA received from other vendors and the Concessionaire due to its management of the Concessions Program. For example, GLAZA received $567,706 in exclusive or official product and service agreements revenue. A portion of the exclusive or official product and service agreement revenues are not currently shared with the Zoo Department.

Free Benefits Provided to GLAZA Members and Business Sponsors. To price membership bundles, GLAZA uses an agreed upon recoup rate. The recoup rate refers to the ratio between the cost of daily admission prices and the cost of an annual membership. It is a measure of how many visits at regular price it would take to recoup the cost of a membership. The recoup rate was 2.0 for FY 2016-17, and prior to July 1, 2016, the recoup rate was 1.9.

While reviewing the FYs 2012 and 2016 Membership, Publications, and Volunteer Programs MOUs we noted that GLAZA’s membership bundles include free guest passes to the Zoo. However, these free guest passes are not factored into the membership price and recoup rate but they entice Zoo patrons to purchase a membership package. It is critical that the membership packages be fairly priced with consideration of admission prices. If the price of membership packages is too low, it can reduce Zoo admission ticket sales. Admission ticket sales are critical because they fund approximately 70% of the Zoo Department’s operating costs; while the Zoo Department receives all revenue from admission ticket sales, it receives only 26% of membership sales revenue.26

For example, as part of GLAZA’s family membership bundle and higher-level membership bundles (i.e., family deluxe, contributing associate, wildlife associate, and conservation associates) GLAZA used to provide up to 12 free guest passes for each bundle purchased.27 GLAZA provided its members between FYs 2014 and 2016 with more than 332,000 free guest passes; 65,500 (20%) were redeemed. These guests are not GLAZA members, thus the Zoo Department could receive a negotiated fee for all free guest pass redeemed. Similarly, the Zoo Department could also negotiate reimbursement for free guest passes redeemed by GLAZA’s business sponsors; however, this would decrease GLAZA’s sponsorship revenues.28 Zoo Department management indicated that it has not requested any reimbursement from GLAZA for the redemption of any free guest passes provided by GLAZA to its members and business sponsors.

26 Based upon GLAZA’s accounting records for shared revenue distributions between FYs 2014 and 2016.

27 According to GLAZA, since FY 2016, the number of free guest passes provided to its members had been reduced and currently, GLAZA offers 2-4 free guest passes to certain membership levels.

28 GLAZA also provides free guest passes to its business sponsors. Based upon information provided by GLAZA, between FYs 2014 and 2016, GLAZA provided 2,314 free guest passes to its business sponsors, of which 227 (10%) were redeemed. Again, the Zoo Department neither requested nor received any reimbursement from GLAZA for these redeemed free guest passes.

Family Membership Bundles May Be Too Incentivized. GLAZA’s family membership bundles do not limit the number of children or grandchildren that can be included in a family membership.29 Coupled with GLAZA’s free member benefits and discount offers, the family and family deluxe membership bundles are favorable. Zoo Department management indicated that they do not review or approve any membership discount promotions offered by GLAZA. However, given that membership package discounts change the recoup rate and can devalue the benefit of purchasing Zoo admission tickets, Zoo Department management should review and approve all discount promotions offered by GLAZA for its membership bundles if they deviate from the prices formally agreed upon by the Zoo Department. Or, if membership package discounts cause a drop to an agreed-upon recoup rate, it could be negotiated into future agreements that GLAZA share a higher portion of the membership revenue with the Zoo Department.

Due to conflicting terms between the Concession Agreement that GLAZA has with the City and the separate contract that GLAZA has with the Concessionaire, the Zoo Department has not received all concessions revenue it was entitled to.

The contract between GLAZA and the Concessionaire has a clause that appears to conflict with the Concession Agreement. The contract clause specifies:

All Zoo and GLAZA staff (full time and part time) and volunteers shall receive a ten percent (10%) discount on food and beverage purchases and twenty percent (20%) on merchandise purchases. GLAZA members shall receive a ten percent (10%) discount on food and beverage purchases and ten percent (10%) on merchandise purchases. Operator agrees to honor these discounts during the term of this Agreement. Gross receipts from these sales will be reported to GLAZA, monthly, but commission payments will not be made on these sales” [emphasis added].

The emphasized term conflicts with different terms in the Concession Agreement between the City and GLAZA, which requires that the City receive 10% of gross receipts from concessions revenue. The Concession Agreement defines gross receipts as the total amount of all sales or the amount charged for the performance of an act, excluding any cash discounts allowed or taken on sales and any sales or use tax added to the purchase price of an item.30 Thus, all sales, less any discounts provided, should be included in gross receipts when calculating the amounts due to the Zoo Department.

29 GLAZA management indicated there are unpublished limits on the total number of children and grandchildren allowed per membership level.

30 The Concession Agreement and Concessions MOU between the Zoo Department and GLAZA do not authorize any exclusion of discounted sales to Zoo Department employees, GLAZA employees, or Zoo volunteers from commissions. Further, the Concession Agreement and Concessions MOU do not specify any discount percentages provided to GLAZA members for food and merchandise purchases.

Upon discussing this discrepancy further, GLAZA management indicated that the Concessionaire has deemed the following sources of revenue as non-commissionable:31

All food purchases by Zoo Department employees, GLAZA employees, and volunteers/docents.

All food purchases for GLAZA or Zoo Department internal events, such as GLAZA Board Meetings, Zoo Commission Meetings, etc.

All food purchases for internal business meetings (client, donor, vendor, etc.) held in the offices of the Zoo Director or GLAZA President.

All snack purchases for Zoo-wide staff meetings.

Zoo Department management indicated they do not review the contracts GLAZA has with the Concessionaire and they were not aware of the conflict between GLAZA’s contract with the Concessionaire and the Concession Agreement.32 Based upon reports provided by GLAZA, the Concessionaire deemed $363,281 of its sales as non-commissionable during FYs 2014 to 2016, which resulted in the Zoo Department being underpaid $36,328 (10% of the sales deemed non-commissionable) in concession revenue due per the Concession Agreement.

Moreover, we found that the Concessionaire has been providing Zoo Department employees, GLAZA employees, and Zoo volunteers with a 50% discount on food purchases that does not correspond to the contract GLAZA has with the Concessionaire. According to GLAZA, this discount is offered because the Zoo is not located near other food outlets and employees/volunteers are not able to drive elsewhere for their meals. However, the 50% discount is much larger than the 10% discount delineated in the contract between GLAZA and the Concessionaire. Any discounts provided by the Concessionaire to Zoo Department employees, GLAZA employees, and Zoo volunteers should be discussed with the OCA to ensure adherence to the City’s rules, regulations, and mandated disclosure requirements. Further, to enhance transparency, all approved and negotiated discounts should be delineated in applicable agreements, MOUs, and contracts.

31 GLAZA confirmed that the Concessionaire is considering all sales to GLAZA members as commissionable.

32 GLAZA management indicated both the Zoo Director and Deputy Zoo Director have attended the GLAZA Board’s Concessions Committee meetings where these contracts were reviewed and discussed.

Recommendations

Insofar as the current governance structure and operational responsibilities exist,

CLA, CAO, OCA, Zoo Department management should:

Renegotiate and clarify all agreements and MOUs with GLAZA, preferably consolidating into a single agreement. Further, consider and evaluate the following items during renegotiations:

a) Revising the revenue-sharing terms by discontinuing the practice of GLAZA’s deducting its expenses from revenues shared with the Zoo Department, and consider allocating a fixed percentage of gross program revenues be distributed between the Zoo Department and GLAZA. If such a revision is not pursued, ensure the agreement(s) clearly delineate the direct and indirect expenses (if any) that are authorized to be deducted by GLAZA from shared revenues.

b) Ensure all applicable agreements with GLAZA, and any contracts GLAZA has with the Concessionaire, have consistent terms and accurately describe any discounts provided to Zoo Department employees, GLAZA employees and Zoo volunteers, while conforming to City rules and regulations and mandated ethics disclosure policies.

The current governance arrangement under which there are contractual agreements between the Zoo Department and GLAZA is, in our opinion, the primary cause for concerns identified by this review. While the relationship between GLAZA and the City has been in place for more than 50 years, it has evolved into more of a partnership, per Zoo Department management, rather than a defined contractor relationship as established by the 1997 Operating Agreement, 1981 Concession Agreement, and subsequent MOUs. Further, some terms within these agreements are ambiguous, or even conflict, especially with regard to revenue-sharing terms, as noted in the previous section.

In 2012, the City attempted to change the Zoo’s governance arrangement from being City managed by the City’s Zoo Director, to being non-government managed by a not-for-profit organization. A consultant retained by the City indicated that a non-government managed arrangement could reduce the Zoo’s costs and increase revenues through a combination of increased flexibility, increased fundraising opportunities, and the gradual transition of City employees to not-for-profit employees through attrition.

The City issued an RFP to have a non-government entity manage the Zoo, and GLAZA’s proposal received the highest score. However, efforts for the Zoo to transition to non-government management ceased when the OCA identified several obstacles, including certain regulations preventing the supervision of City employees by a non-City supervisor.

This review identified several concerns that point to the need to revisit the Zoo’s long-term governance arrangement once again, as discussed below.

The Zoo Department has staffing shortages.

The Zoo Department does not appear to be optimally staffed which may be inhibiting its ability to achieve its vision to be an innovator for the global zoo community, creating dynamic experiences to connect people and animals.

Nearly all Zoo Department managers expressed concerns with staffing, mentioning custodial staff most frequently. Zoo Department managers also mentioned staffing shortages with animal keepers, maintenance construction helpers, and curators. Some of the specific concerns include:

Custodial Staff: There has been a 29% (14 to 10) reduction in custodial staff levels from FY 2008 to FY 2017. Two of the 10 custodians are also assigned to prepare animal feedings at the Zoo’s commissary instead, further compounding the shortage of custodial staffing. With more than 1.8 million visitors to the Zoo each year, custodial staffing appears inadequate, this assessment is further confirmed by surveys of Zoo visitors between FYs 2015 and 2016 who rated the Zoo’s cleanliness lower than visitors to other benchmarked zoos.

Curators: The Zoo Department does not have a horticulture curator or a conservation curator. Without these curators the Zoo Department continues to:

Voluntarily forgo the Zoo’s certification as a botanical garden due to difficulties it has complying with certain mandates (i.e. inventorying botanicals, maintaining logs, and labeling more than 800 different plants and trees at the Zoo).

Lack a formal, comprehensive, and coordinated conservation program focused on animals, plants, public participation, habitat restoration, conservation commerce, and “green” operations.33

Also, Zoo Department management indicated that it requires another education curator to develop a formal school-based curriculum that meets California State Science Standards. The lack of this curriculum reduces the ability of teachers to obtain authorizations for student fieldtrips to the Zoo.34 Based upon the Zoo Department’s Historical Gate Attendance (Appendix V) there has been a 60% decrease (between FYs 2002 and 2016) in attendance by Los Angeles Unified School District (LAUSD) groups, Head Start Program participants, recreation and park center groups, and children under 2.

Part of the decrease may result from the lack of a formal school-based curriculum.35 Further, not having a formal school-based curriculum that meets California State Science Standards may result in less Education Program revenues, as the Zoo Department charges a reduced entrance fee to non-LAUSD school groups. According to Zoo Department management, they recently surveyed teachers to identify their curriculum needs and plan to hire the additional education curator to re-establish a comprehensive school group program with curriculum that will meet California State Science Standards.36

Additionally, the Zoo Department’s Manager of Animal General Care indicated that due to staff shortages, when an animal keeper is on family medical leave, jury duty, worker compensation leave, vacation, or sick leave, it causes the other animal keepers to not only work faster, but also increase everyone’s workload to ensure the entire animal collection is cared for. The Manager of Animal General Care explained that the animal keepers’ workload is already heavy without the additional workload from co-worker absences.37

33 In FY 2017, GLAZA initiated a major effort to establish a $3 million fund to realize the Zoo Director’s desire to establish a formal, comprehensive, and coordinated conservation program for the Zoo. GLAZA’s Special Conservation Action Network Initiative has raised more than $1 million in financial support as of March 2018.

34 Other zoos and aquariums such as the San Diego Zoo and the Long Beach Aquarium have developed formal school- based curriculums and offer tours that meet California State Science Standards.

35 Zoo Department management indicated that the decrease may also result from reductions in school budgets for fieldtrip transportation costs.